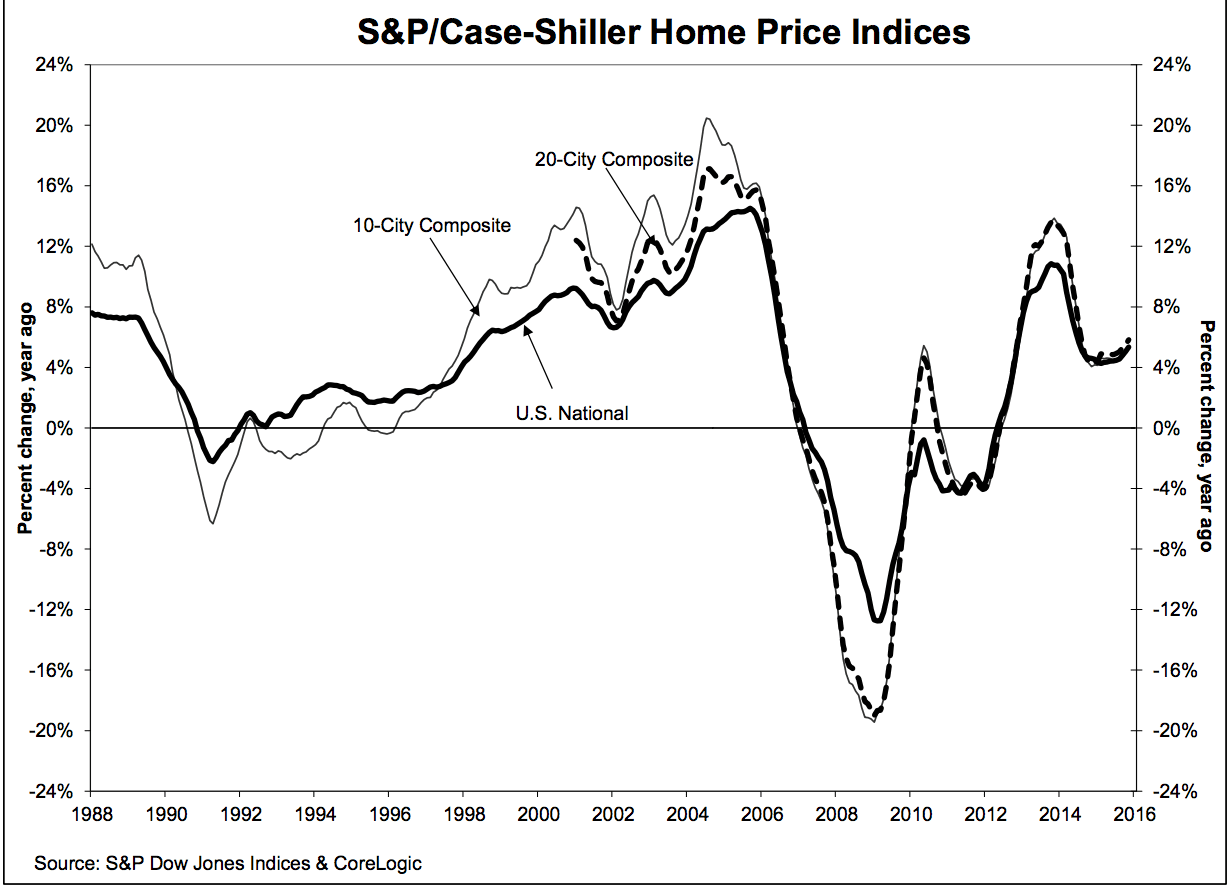

For some, it may be peculiar and perplexing as to why home prices have still increased so far from 2019 to 2020, especially since our current pandemic has caused so much havoc for the U.S. economy. You would automatically think and question that with things being so bad who would be buying and why? It’s the simple fact of supply and demand economics.

Although a segment of the population has either pulled back on considering purchasing due to Covid-19 perhaps because they are currently in limbo due to their business or job status or just don’t have the down payment and or harbor other reasons for their hesitation.

Based on current statistics, however, the demand is still greater than the available supply, which is currently around 4.1 months (as of May), making it a seller’s market. Normal and balanced inventory is six to seven months, moving it more towards potentially being a price-stable or potential buyer’s market and prices would slowly turn in the other direction. There is pent-up demand from those who have been sitting on the sidelines the last few months and have recently re-entered the buying arena, as well as those who are new to the market, such as singles, couples, and young families. The National Association of Realtors says we still have a deficient of upwards of one million more housing units to satisfy our current demand.

The Mortgage Bankers Association is predicting home price increases of 4.3 percent this year, 3.2 percent in 2021 and 2.4 percent in 2022. Zelman and Associates, another prognosticator, sees increases of 3vpercent this year, 4.2 percent next year and 4.6 percent the following year. The National Association of Realtors also follows through with predictions of increased prices of 3.8 percent this year and 2.1 percent in 2021, but does not provide any statistics for 2022. FannieMae, which purchases home loans from larger commercial banks and institutions, predicts increases of 0.4 percent this year and 2.1 percent in 2021, but no statistics for 2022. And Freddie Mac, which purchases home loans from smaller banks and lenders, also predicts smaller increases of 0.4 percent this year, 0.7 percent next year and no statistics for 2022.

With the lack of a sufficient amount of new housing to catch up to the current and future demand going forward as well as the effects of what Covid-19 has done to the supposed non-essential construction industry, building capacity will lag behind demand as long as people continue to come back into the market. It’s obvious prices will continue to increase as our housing inventory stays low and demand continues to increase and stay strong.

Who would have ever thought with all the events occurring here as well as around the globe that the sentiment and mindset for purchasing real estate are still positive? It’s obvious the American Dream of homeownership is alive and well and will continue into the foreseeable future. How else would anyone increase their wealth over the long run with the least amount of risk compared to other more risky investments, while at the same time being able to have a roof over one’s head, build roots within their community, bring up a family, and become their own independent landlord with control over their lives and gain all the benefits and tax deductions and security that 35 percent of the residential population continues to give away to others as renters?

If you are in a position to purchase, and truly understand where your future lies, and currently waiting for prices to come down, this probably is not the most advantageous path to pursue, based on hard and true facts and future projections unless you are earning more than what a home will provide you as far as appreciation and all the benefits that go along with it and the satisfaction of ownership. Settling into a position of owning is a long-term proposition and people may need to revise their original idea of what they were going to buy considering the onslaught of Covid-19. But also consider the cost of buying and the lowest interest rates in 50 years. So taking the plunge today will reap you all the benefits in the future, which may be your greatest and most secure nest egg — as it has been for most — as well as having total say with respect to when and if you want or have to move and not your landlord if you’re in a rental. But if you aren’t ready, then sacrificing, penny-pinching and saving your dollars as much as possible will be the most prudent move you can make before eventually purchasing your first home, condo or coop.

Philip A. Raices is the owner/Broker of Turn Key Real Estate at 3 Grace Ave Suite 180 in Great Neck. He has earned designations as a Graduate of the Realtor Institute (G.R.I.) and also as a Certified International Property Specialist (C.I.P.S). Just email or snail mail (regular mail) him with your ideas and suggestions on future columns with your name, email, and cell number and he will call or email you back. For a consultation, he can be reached by cell: (516) 647-4289 or by email: Phil@TurnKeyRealEstate.Com to answer any of your questions or concerns.