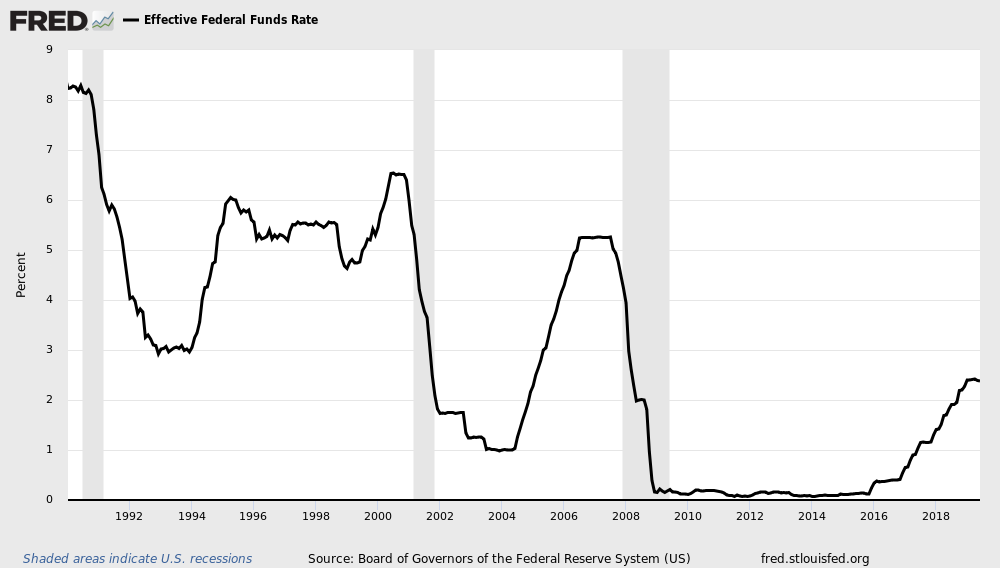

That was the title of a Wall Street Journal editorial back in the ’90s, (when its board wasn’t stuffed with cranks) when Alan Greenspan, in the face of some troubling economic data, announced a 25 basis point rate cut to stave off, or at least slow down, what seemed to be an impending downward turn in the business cycle. It was a sharp, crisp piece — they turned him inside out for what was seen as a weak response to the data. And they were right. a 25-basis-point move to the funds rate is not going to change anyone’s life, with the possible exception of professional bond traders. So Greenspan, in their view, under-reacted.

Fast forward to the Powell era, where the Fed was pilloried for raising rates last December. Personally, and I’m speaking as just one observer from his desk in a very large economy with less than a tenth of the analytical resources others have, I thought it was a mistake to raise rates then, too. But it’s a “mistake” in the sense of putting too much salt on your French fries. It’s not going to kill you, it’s easily digestible, and by dinner, completely forgettable. Unfortunately, the collective voice of what is called “the market” lost its mind. So they saw this as an overreaction. The pundit class immediately started plugging in the “possibility” of two or three more hikes this year.

In the ensuing months, a few unexpected things came the Fed’s way, including a tariff war managed by a feces-throwing chimpanzee, and what appears to be some “unsointanty” caused by Brexit and the effects on the economies of the EU. Convenient excuses to backtrack this week, but hardly a reason. Then the bipolar effects caused by the followup in Powell’s comments. The market, having been well prepared for the cut, didn’t react on the announcement. Once Powell stated this wasn’t the beginning of a longer term trend in rate reduction, it immediately sold off. The next morning, by the open, we were back to where we were before the chair’s comments. And on it goes.

And now, in the midst of dozens of earnings announcements, which are far more telling about the direction of the economy than a cut in rates that will end up saving you $6.25 a month on your auto loan, I am swimming in blather about the meaning of all this. So why is so much bandwidth and commentary exhausted on these minuscule moves in the cost of credit? It’s a problem I’ve mentioned before: We lay TOO much at the feet of the Fed, and while these inputs are certainly critical, we ignore everything else we should be doing to help the economy and its participants, and then complain that things aren’t getting any better in real terms for real people. But it’s so much easier to focus media heat on personalities instead of telling more complex stories that take up time, or explore initiatives that may take months, or even years to change the trajectory of the economy.

Cheaper credit is a great way to get people spending and building. But that’s it. Once you’ve accomplished that task, a quarter of a point this way or that is utterly meaningless. It does nothing for the real problems of stagnant wages, a predatory health care system that has strip mined the wealth out of the country’s citizens, or the growing divisions in the spoils of our economic growth. There will no news conferences for those issues, and we can look forward to being waist deep in anger and frustration until we start focusing on what matters.

I’m not optimistic.

Donald Davret

Roslyn